At the IT Press Tour, StorPool argued that sovereign infrastructure, pressure to migrate from VMware, and hardware shortages are converging—and that software-defined storage is the structural solution.

At the IT Press Tour in Sofia, the leadership team of Bulgarian storage provider StorPool Storage outlined four converging trends that are reshaping enterprise IT infrastructure. The company believes that its software-defined storage platform is structurally suited for each of them.

Founded in Sofia in 2011, StorPool describes itself as a provider of block-level software-defined storage (SDS) for private and public clouds, hosting companies, and large enterprises. The company employs around 60 people, operates across more than 30 countries, and is founder-owned and profitable — a point its CEO Boyan Ivanov returned to more than once during the briefing as evidence of sustainability rather than venture-fuelled growth. StorPool claims to serve more than one million end users through its customers, which include infrastructure companies running workloads for organisations such as NASA, CERN, and Deutsche Börse Group.

The platform itself delivers block storage software that runs on commodity server hardware, positioning itself as a replacement for traditional storage area networks (SANs), all-flash arrays, and competing SDS products including VMware vSAN, Dell PowerFlex, and IBM Storage Ceph. Key technical specifications cited during the briefing include sub-100-microsecond latency, measured availability exceeding 99.999 percent, and the ability to scale online from 10 terabytes to more than 50 petabytes without interrupting running workloads. StorPool also includes what it calls VolumeCare for backup and a Disaster Recovery Engine as built-in components, reducing dependency on third-party tools.

THE VMWARE FACTOR

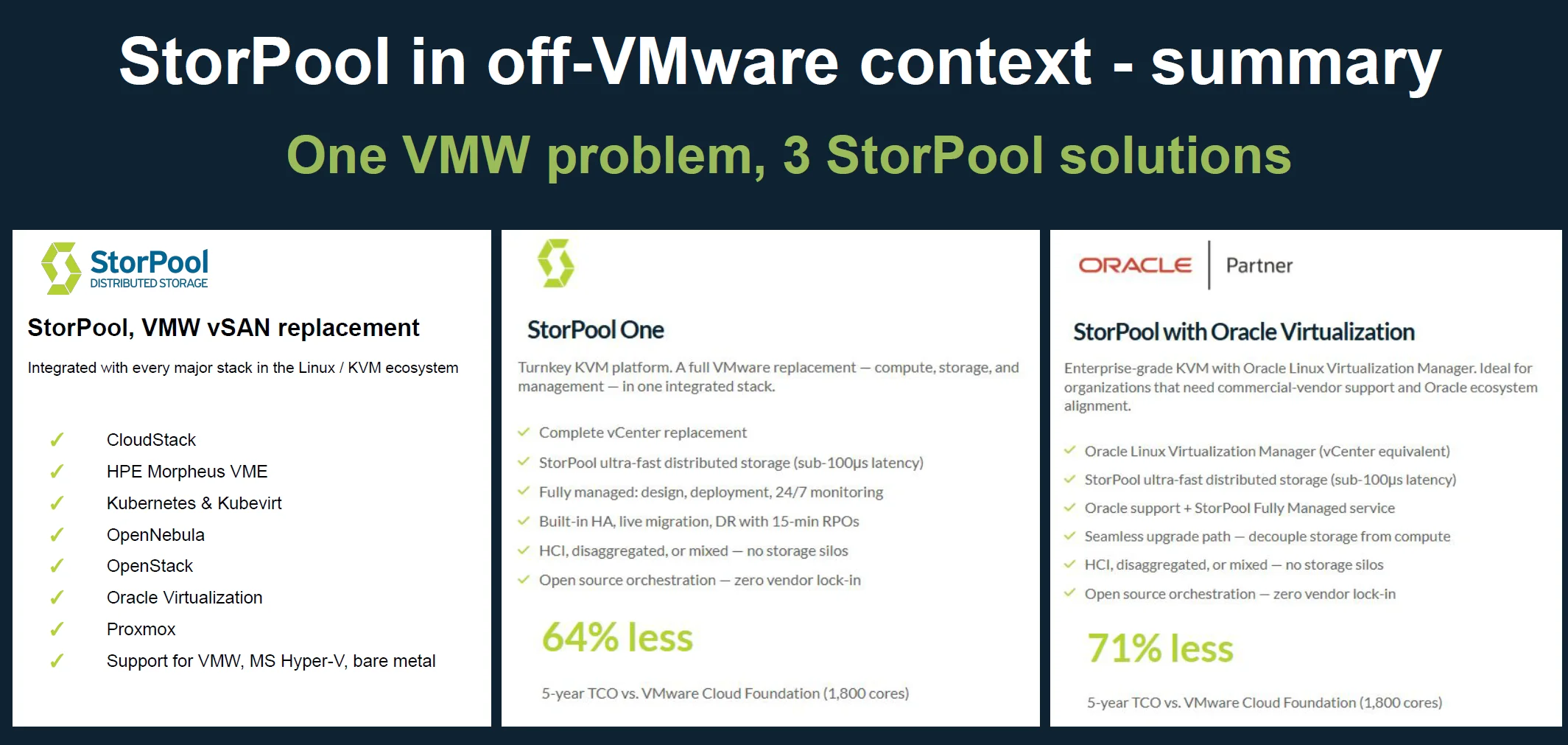

The most extensively discussed trend was what StorPool calls the VMware exodus. Following Broadcom’s acquisition of VMware, many customers faced licence restructuring that reportedly increased costs by a factor of ten for some deployments. For cloud service providers and hosting companies operating on thin margins, the impact has been acute. StorPool’s internal modelling suggests that most migrations from VMware will be concentrated in the period between 2025 and 2027, after which the volume of active migrations is expected to decline significantly.

The company presented three distinct offerings for customers leaving VMware. The first is StorPool Storage deployed as the storage layer in a KVM-based stack, functioning as a direct replacement for vSAN alongside open-source hypervisor options such as Proxmox or Oracle Linux Virtualization Manager, and cloud management platforms including OpenStack and CloudStack. The second is StorPool One, announced on March 19, 2026, which bundles compute, storage, and management into a single integrated stack and aims to eliminate the integration complexity that makes post-VMware migrations technically demanding. A five-year total cost comparison shown during the briefing placed StorPool One at approximately 1.13 million dollars against 3.15 million dollars for VMware Cloud Foundation on an 1,800-core deployment — a stated saving of around 64 percent. The third offering, developed in partnership with Oracle, incorporates Oracle Linux Virtualization Manager and targets enterprises that require commercial support and alignment with the Oracle ecosystem. This configuration was cited as approximately 71 percent less expensive over five years compared with VMware Cloud Foundation.

Ivanov acknowledged that VMware remains technically without a direct peer. The point, he argued, is not capability parity but cost tolerance: organisations that were content with VMware’s product could no longer justify its post-acquisition pricing, and were seeking alternatives that offered sufficient functionality with comprehensive support and lower total cost.

EU DATA SOVEREIGNTY AND CLOUD REPATRIATION

The second trend StorPool addressed was European data sovereignty and the broader movement toward sovereign clouds. Ivanov described a call he received from a contact at the European Commission who noted that core EU systems were running on Chinese hardware and US software — a realisation that, in his telling, came later than it might have. The observation reflects a wider shift in procurement thinking across European public institutions and regulated industries, where questions about data jurisdiction, vendor nationality, and resilience to geopolitical disruption are being asked with more urgency than previously.

StorPool’s positioning here rests partly on geography. As a European company headquartered in Bulgaria with no US parent or majority investor, it can make a credible claim to non-American provenance — a factor that the company says is being raised explicitly by prospective customers in Europe, the Middle East, and Asia who are actively seeking to reduce exposure to US-based vendors.

Beyond its corporate structure, StorPool cited its participation in the EuroStack Pack initiative, a consortium effort to assemble a full European-sourced infrastructure stack covering hardware, storage, network, compute, and management layers. StorPool and Cubbit were noted as the storage-layer participants alongside SUSE, which provides hypervisor, compute, and management platform components, and Cilium for networking.

AI INFRASTRUCTURE

AI was addressed as a third trend, though the company was measured in its claims. Ivanov noted that the market for AI infrastructure spending is effectively concentrated among a small number of very large organisations — a list he abbreviated to around ten entities globally — while the majority of businesses use AI as consumers of services rather than builders of infrastructure. For StorPool, the relevant use cases are inference workloads, retrieval-augmented generation (RAG), and vector databases, all of which benefit from low-latency block storage. The company cited several customers operating GPU-as-a-service platforms powered in part by StorPool, including Cloudalize and Redmond.ai.

HARDWARE SCARCITY AND RESOURCE EFFICIENCY

The fourth trend discussed was the combined effect of hardware price inflation and supply chain constraints. StorPool’s CTO noted that 40 percent of helium and 45 percent of neon — materials essential to semiconductor manufacturing — are produced in the Middle East, where export flows have been disrupted. Chip production capacity through mid-2028 was cited as already committed, with no slack available in the near term. The practical consequence for infrastructure operators is that buying new hardware to accommodate growth is less viable than it was, and software that extracts more from existing hardware has corresponding value.

StorPool’s response to this environment is threefold. First, the platform’s lightweight footprint — claimed at 10 to 15 percent of host CPU and RAM in converged configurations — allows existing servers to support additional workloads. Second, by replacing less efficient storage software, organisations can reclaim compute and storage resources that were previously consumed by the storage layer itself. Third, StorPool’s I/O management design was reported to consume only 16 percent of SSD endurance over five years of transactional database workloads in one documented deployment, extending the usable life of drives beyond their nominal warranty periods.

A BROADER ECONOMIC ARGUMENT

Across all four trend areas, StorPool made a consistent argument: that optimising storage has compounding effects on the surrounding infrastructure stack. Fewer storage nodes mean fewer network ports and switches. Lower resource consumption per node means higher virtual machine density per rack. Higher density means fewer racks, less power, and potentially fewer data centres. The company cited case studies in which customers reduced their data centre footprint from thirteen sites to five, or from three equipment racks to half a rack, through converged infrastructure deployments powered by StorPool.

Customer examples cited in the briefing include Atos, which was described as having eliminated planned downtime and hardware refresh cycles; CloudSigma, which attributed a 15 percent margin improvement to its storage architecture; Dustin, a Nordic IT services company, which reduced its storage management headcount from 50 to 5; and Namecheap, which achieved a 60 percent increase in virtual machine density per rack.

The company characterised its approach as a shift from traditional IT operations — characterised by functional silos, manual processes, and scheduled maintenance windows — toward a continuously operating, API-driven model in which storage management becomes largely automated. In practice, this means that StorPool’s customers have moved from periodic maintenance windows, often difficult to schedule, to systems that run continuously without planned downtime.

StorPool’s geographic revenue split was described as approximately 50 percent Europe, 30 percent North America (including Canada), and 20 percent rest of world. The company does not currently operate through a broad reseller network, conducting most business directly with customers, though it partners with Oracle and Hewlett Packard Enterprise for specific offerings.

Dr. Jakob Jung is Editor-in-Chief of Security Storage and Channel Germany. He has been working in IT journalism for more than 20 years. His career includes Computer Reseller News, Heise Resale, Informationweek, Techtarget (storage and data center) and ChannelBiz. He also freelances for numerous IT publications, including Computerwoche, Channelpartner, IT-Business, Storage-Insider and ZDnet. His main topics are channel, storage, security, data center, ERP and CRM.

Contact via Mail: jakob.jung@security-storage-und-channel-germany.de